- 10X Capital

- Posts

- The 10X Capital Newsletter

The 10X Capital Newsletter

What will it take for an LP to Re-Up into my next fund?

David Weisburd

March 26, 2024

The 10X Capital Podcast is a podcast where David Weisburd and Erik Torenberg interview the world’s top Venture Capitalists and their Limited Partners.

Today’s Agenda 📋

⭐️ Today’s Spotlight: What makes an LP Re-Up (or not)?

✍️ Top Posts of the Week

📈 Chart of the Week

🔧 Emerging Manager Tools

Recent episodes 🎙

"The 10X Capital Podcast" with David Weisburd and Erik Torenberg | Startups, Venture Capital, and Limited Partners:

Listen on Apple Podcasts or Spotify

Listen on Apple Podcasts or Spotify

This week’s Liquidity Podcast 💰

Every week, we’re going to cover a topic that is widely acknowledged but often misunderstood in the venture industry.

So without further ado, today’s topic: What makes an LP Re-Up (or not)?👇

What makes an LP Re-Up (or not)?

Emerging managers and LPs both expect to enter a long-term relationship with each other when the first check is written. Ideally, this relationship spans several decades.

In fact, this is how large franchises are built in the space (watch my David York interview where he discusses step by step how he raised $8 Billion from LPs over several decades).

This begs the question, what will it take for an LP to re-up into my next fund?

Most institutional LPs invest across many managers. They dedicate significant amounts of time and resources in order to diligence each new manager, conducting reference checks, and determining how that new manager fits into their allocation strategy.

If a manager makes it through an LP’s vetting process, and the LP decides to write a check into their first fund together, the LP wants to stay together for the long term. All else equal, the LP really wants to re-up into your subsequent funds. But, this is happening less and less.

Unfortunately, circumstances change.

So the real question is, what would make an LP not want to re-up?

For emerging managers, it’s NOT the performance from the previous fund. This is a common misconception amongst emerging managers, but performance is NOT the short-term reason why LPs do not re-up, that is because it takes at a minimum until Fund III for performance to actually show and for early bets to materialize.

It’s simply too early to determine Fund I's performance when an emerging manager is out and raising Fund II.

LPs therefore decide not to re-up due to these three core reasons:

Change in fund size

“Your fund size is your investment strategy” is a long-echoed saying in the asset management world. This is because your fund size will determine the size of checks you’re writing, whether you’re leading rounds, and other mechanics involved with sourcing, picking, and winning the best deals. All else being equal a fund that grows too large is a fund that changes from an Alpha fund to a Beta fund, and Beta is not what many LP’s are looking for.

Strategy creep

Emerging managers often expand the scope of their investment thesis as they raise subsequent funds. This can mean investing in new verticals outside of your expertise or funding companies in later or earlier stage rounds. These changes to your core thesis as a manager can lead LPs to opt-out of future vintages or at a minimum re-underwrite you and your capabilities of executing the new strategy.

Management team shake-ups

When an LP backs a fund, they’re betting on the manager or group of managers at the VC firm to generate alpha. Because of this, significant personnel changes at the management level of the VC firm can lead to LPs deciding not to re-up.

Other than manager-related changes, LPs might not be in a position to re-up because of changes on their side of the table, or issues that are widely covered such as the “Denominator Effect” but this is a topic for a future newsletter - until then.. 🫡

—------

If you found this helpful, please forward it to a friend. If you are that friend, subscribe here.

Next week, we’ll be discussing how LPs deliver value to VC managers

Top posts of the week ✍️

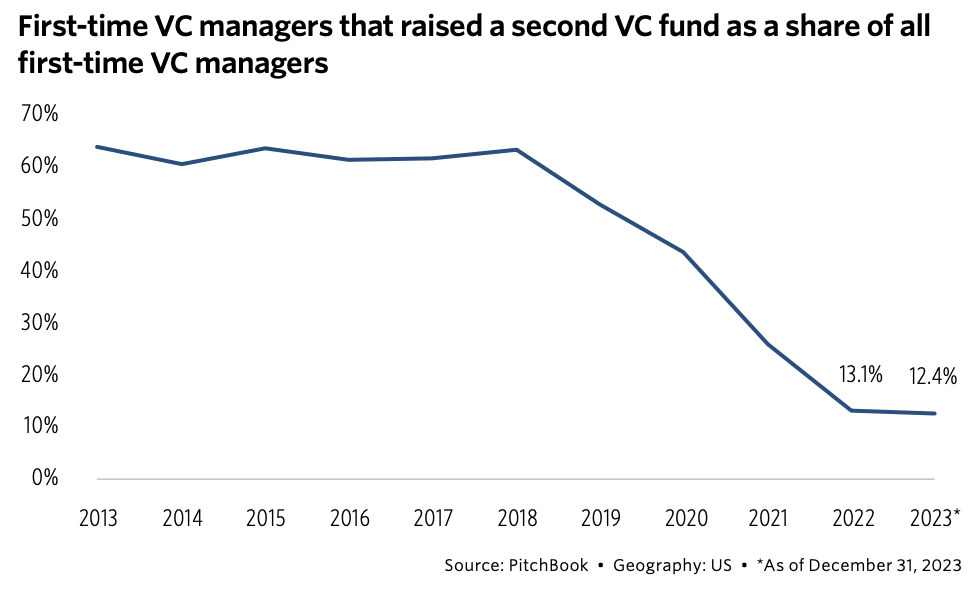

Chart of the week 📈

Emerging manager tools 🔧

Chris Harvey for fund counsel

Reach out to Chris at [email protected].

AngelList for fund administration

Get in touch by emailing the team at [email protected].